Search

From Green Investments to Digital Currency: Students Discuss Innovations in the World of Finance

August 16, 2013

Like any other field, the world of finance has also witnessed a number of path breaking innovations. From physical share trading to demat trading, from long queues in banks to ATMs and mobile banking, from barter trade to forex, from coins to digital currency…the list is long!!

Members of Centre for Management’s finance club Finacle got together to discuss some of these financial innovations. Teams of two each pictorially presented innovations in the financial field and their future promise.

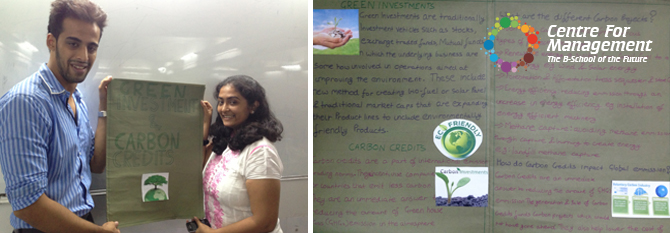

Semester III PGDBM student Khalid Memon along with Semester III PGDBM student Shravya Rao talked about green investments. They explored how green companies are attracting investors, venture funds and private equity into their businesses. Rising environmental concerns have created a situation where any eco-friendly process, product or technology is always welcomed. Also, companies are trying to earn more carbon credits which are permits that allows the holder to emit one ton of carbon dioxide for each credit. Credits are awarded to countries or groups that have reduced green house gases below their emission quota. The team noted that India could be a leading supplier of carbon credits to other countries like Europe which are typically low on carbon credits. Corporations and PSUs are also eyeing the carbon credit business as it can be easily traded on the exchange.

Kartik Kothari and Manali Jain presented the pros and cons of digitalization of currency

Kartik Kothari and Manali Jain presented the pros and cons of digitalization of currency

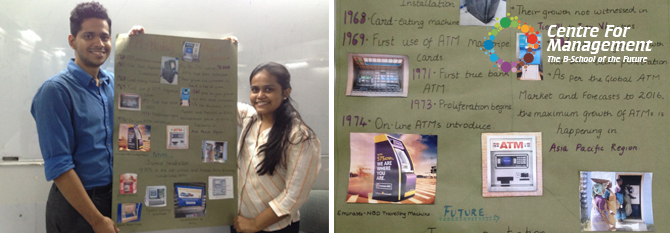

Students Sagar Nathani and Tanvi Gada took the club members through a historical journey of ATMs

Students Sagar Nathani and Tanvi Gada took the club members through a historical journey of ATMs

Their classmates Kartik Kothari and Manali Jain presented the pros and cons of digitalization of currency. Prevention of theft, tracing black money, smoother transactions, better fund accounting were stated as advantages, whereas low internet penetration, the number of people without bank accounts, unawareness, regulatory framework etc. were identified as the flip sides to this trend. The duo also pointed out that an innovation like Google Wallet has a long way to go in a country like India. Moreover, they came up with a solution as to how digital currency and cloud computing technologies can be merged for better digital transactions.. Indeed, digital currency could be a giant leap in the field of financial innovation. The RBI will have less to worry about… or maybe more! Who knows…..?

Students Sagar Nathani and Tanvi Gada took the club members through a historical journey of ATMs. ATMs, which today seem commonplace to us, were once a distant dream. Even today, they are merely used for cash withdrawals, although they are capable of handling a large number of financial transactions. Going forward, the team anticipates that branded restaurants, large food chains and shops will have their own ATMs where one can swipe a card and the payment is directly made to the seller. They also pointed that in the future, all transactions will be card-less as mobile phones will be merged with ATMs to verify the identity of the user. The team also highlighted that for ATMs to be a success, better reach in rural areas is critical. Just as mobile penetration in rural and semi-urban areas has been increasing, ATMs too can be made accessible in these places if banks are given incentives to do so. There’s no doubt that ATMs have reduced bank queues to a great extent, but a lot more technology needs to be incorporated to establish a more widely acceptable model for innovative banking.

Finally, Semester III PGDBM student Danish Shaikh got the club members thinking about mobile banking innovations. He went on to say that it’s only mobile banking that will lead to paperless transactions in the Indian banking industry. India has approximately 929.37 million mobile phone subscribers. So the reach of mobile banking is extensive. With the advent of smart phones, mobile banking seems inevitable. Rural customers can use simple messages to check balances and speak to customer care executives. Danish explained that in the future, funds could be exchanged between two accounts through two different handsets just like exchanging an SMS or a Bluetooth file. It was also highlighted that the entire cycle of cheque clearing – both local and outstation – which takes at least 3 days, can be brought down to just a few seconds through mobile banking.