Search

Reverse Mortgage: What is it? How does it Work?

April 26, 2017

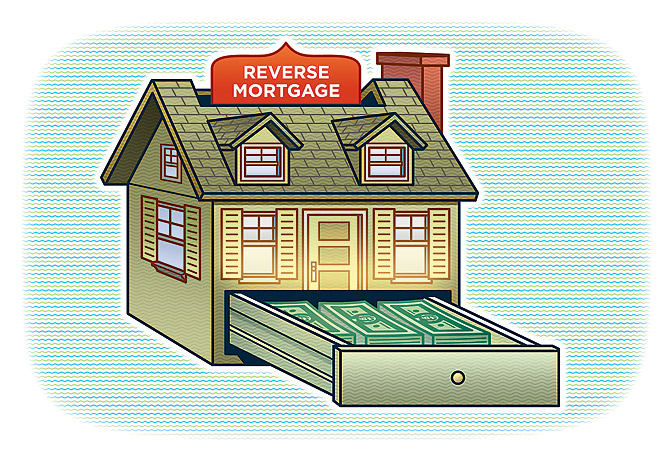

In a standard mortgage, a person who can’t own a property himself gets a home loan to fund the purchase and repays it in the form of periodic payments. A reverse mortgage is exactly the opposite. Thus, in this, a person who already owns a house receives periodic payments from the bank by offering the property as collateral.

A reverse mortgage is ideal for senior citizens who need money in their twilight years to take care of themselves. This is because after their demise their property can be sold off by their heirs or the bank for the settlement of the loan.

Here is how a reverse mortgage works:

1. The borrower mortgages their house to the lender (bank or another financial institution).

2. The borrower receives monthly/quarterly payments from the lender during the term (or until they pass away). During this period, the rights to the property rest with them.

3. When the borrower dies, the house loan (reverse mortgage) is paid by the legal heirs, after which they are provided the property rights. In case the heirs are not willing to repay the loan, the bank seizes the property and sells it off to recover the money.

Key points to remember:

-

A reverse mortgage is usually available to only the senior citizens (above 60 years of age).

-

The maximum period or reverse mortgage is usually 15 years. However, some banks may offer a longer period, such as 20 years.

-

Since the funds received through a reverse mortgage is considered as a loan and not an income, they are not taxed.